Problem

Open standards-based Cloud Entitlements Service (OCES) is the strategic authorization platform for Cloud-native applications across Goldman Sachs. OCES uses Open Policy Agent (OPA) as the policy engine. OCES provides a centrally managed, externalized authorization service, that enables developers to define, manage, and enforce entitlements and policies for their applications.

OPA was originally designed to be used as a lightweight policy engine that can be co-located and integrated with an application. However, running it as a policy engine of an externalized authorization service introduced new challenges related to secured and efficient policy delivery.

This blog post describes how the OCES platform evolved to addresses these challenges.

Overview of OCES

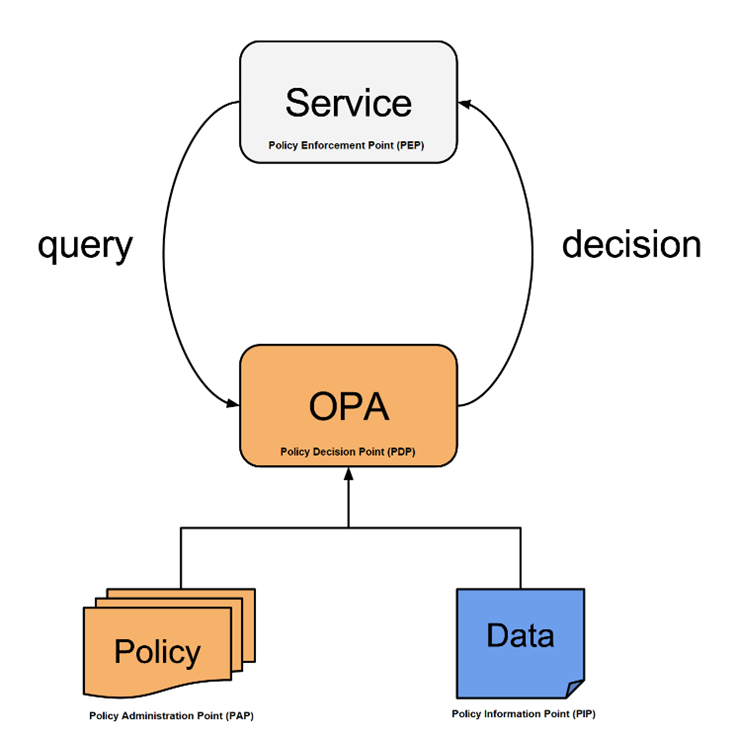

OCES is powered by Open Policy Agent (OPA). OPA is an open source, general-purpose policy engine that unifies policy enforcement across the stack. OPA provides a high-level declarative language (called Rego) that lets you specify policy as code and simple APIs to offload policy decision-making from your application. These Rego policies, along with the reference data, are used to make authorization decisions. OCES uses several governed reference data sources as the reference data, whereas the Rego policies are authored by business units, referred to as tenants in OCES. It separates policy management from the application lifecycle and delegates access control decisions to an external decision point.

Figure 1: OPA policy engine

The multi-tenancy concept in OCES is modeled on business units (e.g., Global Investment Research, Transaction Banking, etc.), designed to enforce a vertical separation across the OCES ecosystem. This separation ensures that every entity in OCES (e.g., reference data, Rego policy, deployment) is mapped to an OCES tenant, which is crucial for:

- Restricted visibility of reference data and Rego policies

- Independent infrastructure and operations

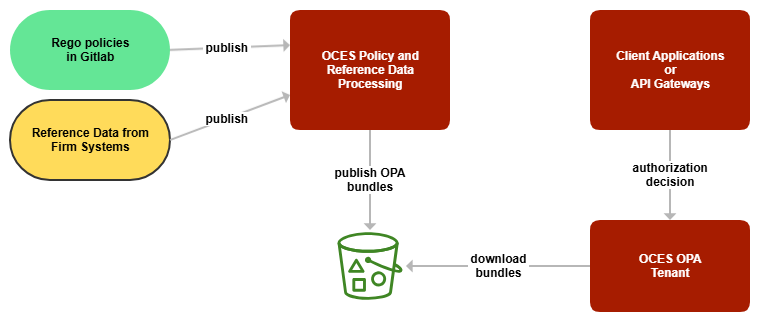

Here’s a 10,000-foot view of OCES:

Figure 2: 10,000-foot overview of OCES architecture

The Rego policies are authored in Gitlab and published to OCES Core (OCES Policy and Reference Data Processing) for processing. Using Gitlab facilitates inherent version control, unit testing, approval workflow and audit features. The policies are bundled into a tar archive and stored in S3. The reference data from various sources is published to OCES Core for processing. They are bundled into a tar archive and stored in S3.

OCES OPA tenants download these bundles and load them in-memory. OPA polls S3 every minute (configurable) to check if fresh bundles are available. OPA limits the maximum bundle size to 1 GB. In-memory bundles allow OPA to take quick (<10ms) decisions on the authorization requests sent by client applications. However, the low latency comes at the cost of high memory utilization, as OPA memory requirement is ~200x of the bundle size.

OCES OPA tenant deployments support the heterogeneity of use-cases across the firm. OCES tenant deployments are multi-cloud (currently deployed in AWS and GCP) and support both – central or sidecar deployment model based on the latency budget. A detailed overview is available in a previously published blog post on Cloud Entitlements Service.

The next section describes the challenges in using OPA in a centrally managed externalized authorization service.

Challenges In Using OPA For Externalized Authorization Service

OPA was originally designed to be used as a lightweight policy engine that can be co-located and integrated with an application - as a sidecar, host-level daemon, or library. This pattern enables fast authorization decisions but isn’t suitable for a centrally managed authorization service due to below reasons:

- Application teams need to deploy and manage OPA servers and application developers need to build OPA competency.

- The OPA servers for different applications can have different OPA versions and configurations, rendering Rego policy management difficult. For example, a policy bundle built with a higher OPA version can fail to load in an OPA server running a lower OPA version.

- Audit and regulatory overhead on applications. For example, regulation requires storing the OPA decision logs for 7 years. Application teams would also be responsible for infrastructure and process audit, Business Continuity Planning evidence, Tech Risk design reviews, etc.

Conditioning OPA to make it suitable for OCES required:

Scaling the OPA servers

The OCES multi-tenancy model ensures that authorization query traffic is bound at tenant level, limiting the blast radius to a specific tenant.

Within a tenant, AWS autoscaling for ECS is configured to horizontally scale the OPA cluster size based on the usage.

Scaling the OPA bundle delivery

While AWS autoscaling provides an easy solution to scale OPA servers, the challenging part is to scale the OPA bundle delivery.

Bundles contain the Rego policies and reference data. As OPA servers load the bundles from the S3 bucket, the challenge is to ensure that the Rego policies and reference data is delivered to OPA in a quick and secure way.

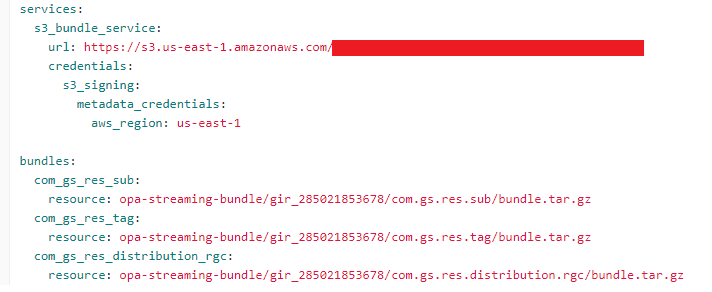

In the initial OCES launch (Policy Publication v1), the bundle delivery process required manual onboarding and deployment for each policy onboarding, which wasn’t scalable.

Figure 3: OPA configuration with each Rego policy as a bundle

The next section describes how we iteratively optimized the Rego policy bundle delivery.

Optimizing the Policy Bundle Delivery

Policy Publication v1 had two major issues:

- Each Rego policy had to be onboarded individually.

- Every onboarding needed a deployment.

Along with that, TechRisk observed that there was no standard integrity check of the Rego policies (i.e., The policy was not manipulated between authoring and enforcement).

The next section describes how OCES solved these issues with bundle discovery and signing.

OPA Bundle Discovery and Signing

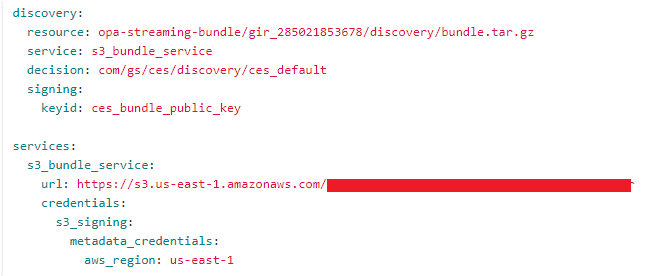

OPA provides a discovery feature which helps you centrally manage the OPA configuration. When the discovery feature is enabled, OPA will periodically download a discovery bundle and process it to generate the rest of the configuration.

Building onto the discovery feature provided by OPA, OCES launched a new version of policy publication (Policy Publication v2). The new policy publication pipeline didn't require onboarding and deployment of each Rego policy. Clients would only need to onboard their Rego Gitlab repository once. After that, they could publish any number of Rego policies without any onboarding.

Moreover, as soon as the Rego policies were published, they were immediately made available to the respective OCES OPA tenants, without any deployments.

Figure 4: OPA bundle discovery configuration

OPA supports digital signatures for policy bundles. Specifically, a signed bundle is a cryptographically secure OPA bundle that includes a file named “.signatures.json” that dictates which files should be included in the bundle and what their SHA hashes are.

OCES Policy Publication v2 used this standard bundle signing mechanism to sign bundles. During creation, bundles are signed with a secure private key. In the OCES OPA tenants, a public key is used to verify the integrity of the bundles.

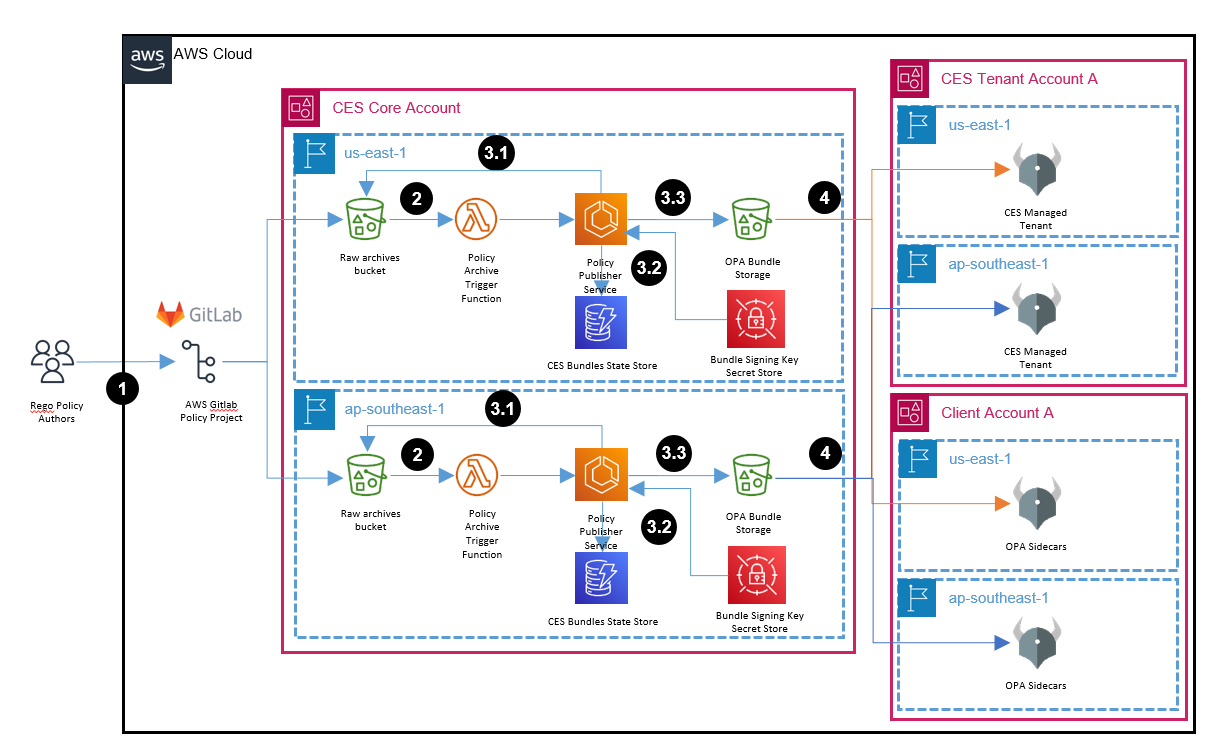

Figure 5: Architecture post bundle discovery and signing.

- (1) Authored Rego policies are uploaded as an artifact to a S3 bucket

- (2) Each upload triggers a lambda function, which calls the policy publisher service to notify it of an upload.

- (3.1) Policy publisher downloads the artifact and (3.2) is configured with the private key used to sign the bundles at startup. (3.3) The policy publisher stores the meta-data in DynamoDB, creates a bundle out of the artifact and uploads it to S3. It also updates the discovery bundle for each tenant if required.

- (4) OPA polls S3 for updates on the discovery bundle and regular bundles

Policy Publication v2 was widely adopted and OCES clients appreciated the seamless, fast, and secured bundle delivery.

However, some clients reported that their Rego policies were taking too long (~30 mins) to become available after publication.

The next section describes how we diagnosed and solved this delay in bundle delivery.

OPA Bundle Consolidation

The first diagnostic step was to profile the delay in bundle delivery. Using the Prometheus metrics published by OPA servers, we observed that OPA was taking a long time to activate the bundles after downloading them from the S3 bucket. Policy Publication v2 pipeline created one OPA bundle for each Gitlab repository (pipeline v1 created one bundle for each Rego policy).

We ran many tests and confirmed that the delay was only observed in the OCES OPA tenants which had a comparatively high number of Rego repositories onboard.

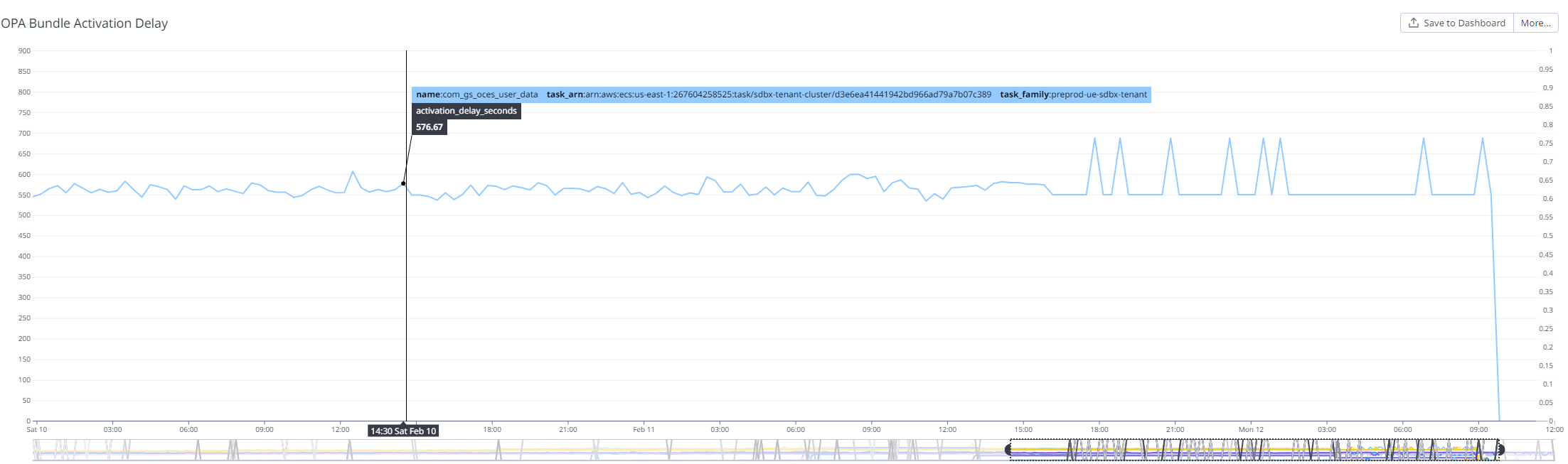

Figure 6: The ‘activation_delay_seconds’ is the number of seconds OPA took to activate a bundle after it’s downloaded. Ideally, this lag should be near-zero, but it was observed to be nearly 10 minutes.

We shared these results with OPA support team and they concluded that though OPA supports multiple bundles, it’s not optimized to efficiently activate them. The root of the issue is that when OPA activates a new bundle, it also compiles all the existing activated bundles. As this compilation is expensive, there exists a tipping point, dependent on the number and size of the bundles, after which the time taken by OPA to activate the bundles will increase unsustainably.

The only path forward was to consolidate the bundles. This meant creating one bundle per OCES OPA tenant, comprising of all the reference data and Rego policies applicable to the tenant.

Bundle Consolidation Challenges

There were several risks and challenges in consolidating the bundles:

- Blast radius of a bad Rego policy – OPA fails to activate a bad bundle. Prior to consolidation, this would only affect one bundle. With consolidation, this would affect the whole tenant, causing a wide outage.

- Policy namespace conflicts – Rego policies across repositories may have namespace conflicts. This would result in a bad bundle.

- Separate bundle generation process for reference data and Rego policies – The reference data and Rego policies bundles were generated by two separate processes. To generate a consolidated bundle, all these individual bundles needed to be packaged as a single valid bundle efficiently.

Bundle Consolidation Design

We first introduce the concept of an aggregate state. An aggregate state is maintained for each OCES OPA tenant, that contains all the individual Rego policy directories and data bundle directories within it. A metadata file contains additional information about the aggregate state.

The purpose of this aggregate state is to provide a staging area before consolidating the bundles. Before generating the consolidated bundle from the state directory, it must satisfy a series of invariants.

These invariants are designed to ensure that the consolidated bundle is always healthy. The invariants are:

- No two policy projects in the aggregate should share a common Rego package.

- Example - If spr_123456 contains a Rego package "com.gs.hcm" and spr_109077 contains a Rego package "com.gs.hcm.operations", the resulting aggregate state becomes unhealthy because the package names are overlapping.

- No two Rego repositories/reference data bundles should have any conflicting documents. This invariant is similar to #1 but applies to path conflict between static data documents.

- No import errors across different Rego policy repositories.

- Example - OCES provides the "com.gs.oces.appdir_client" Rego policy as a library for AppDir authorization calls, which is imported in the Rego policies of applications. If this dependency is missing in the consolidated bundle, it will result in an import error and fail to activate.

The consolidated bundle is run in an OPA server before publication. If the bundle is loaded and activated successfully, only then it is published to S3. This ensures that OCES OPA tenants always receive a healthy consolidated bundle.

Consolidating the reference data and Rego policy bundles at scale requires orchestration, which can be implemented with event streaming.

In this design, every policy publication pipeline trigger or reference data bundle change is modeled as an event, which is published to a Kafka topic. The events are consumed, and the aggregate state is modified accordingly. A successful modification, satisfying the invariants, results in a consolidated bundle.

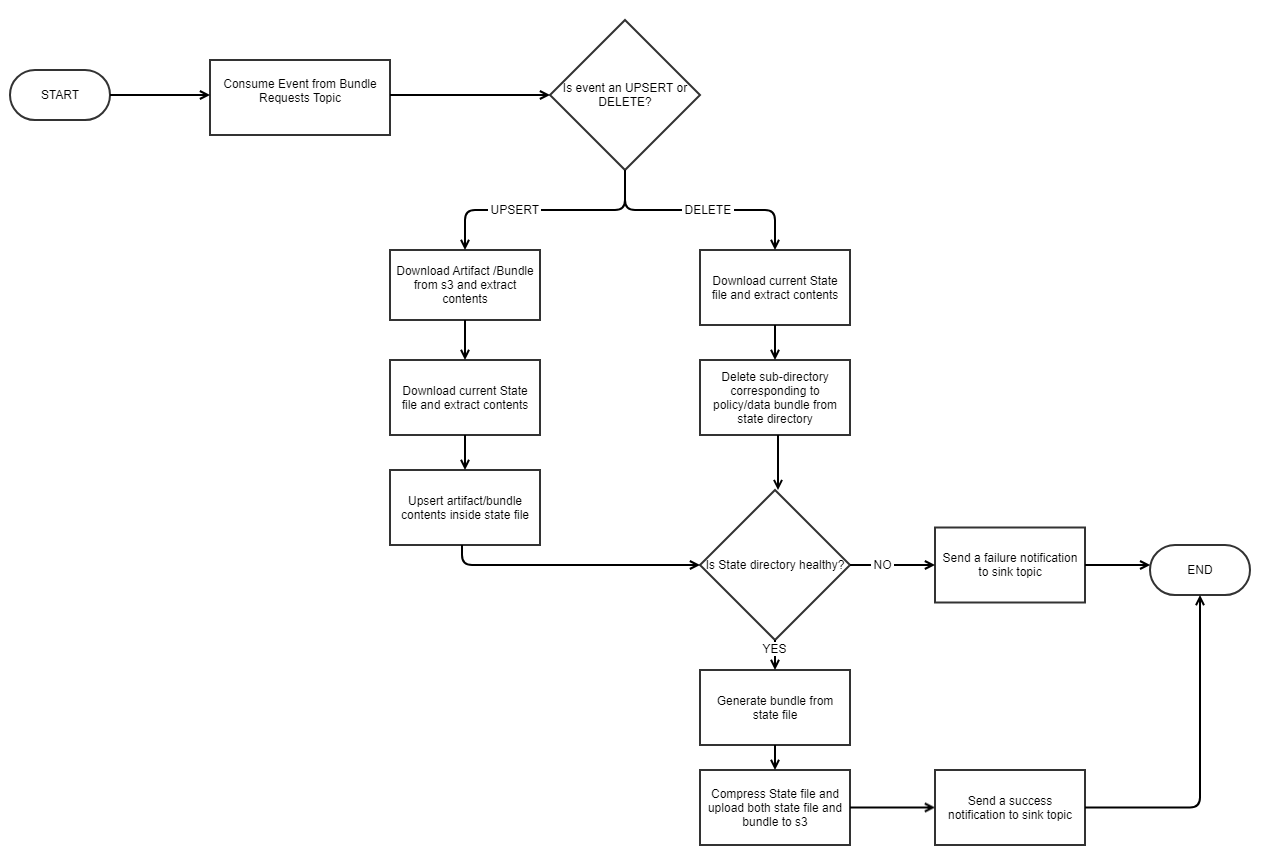

Figure 7: Process flow diagram for bundle consolidation

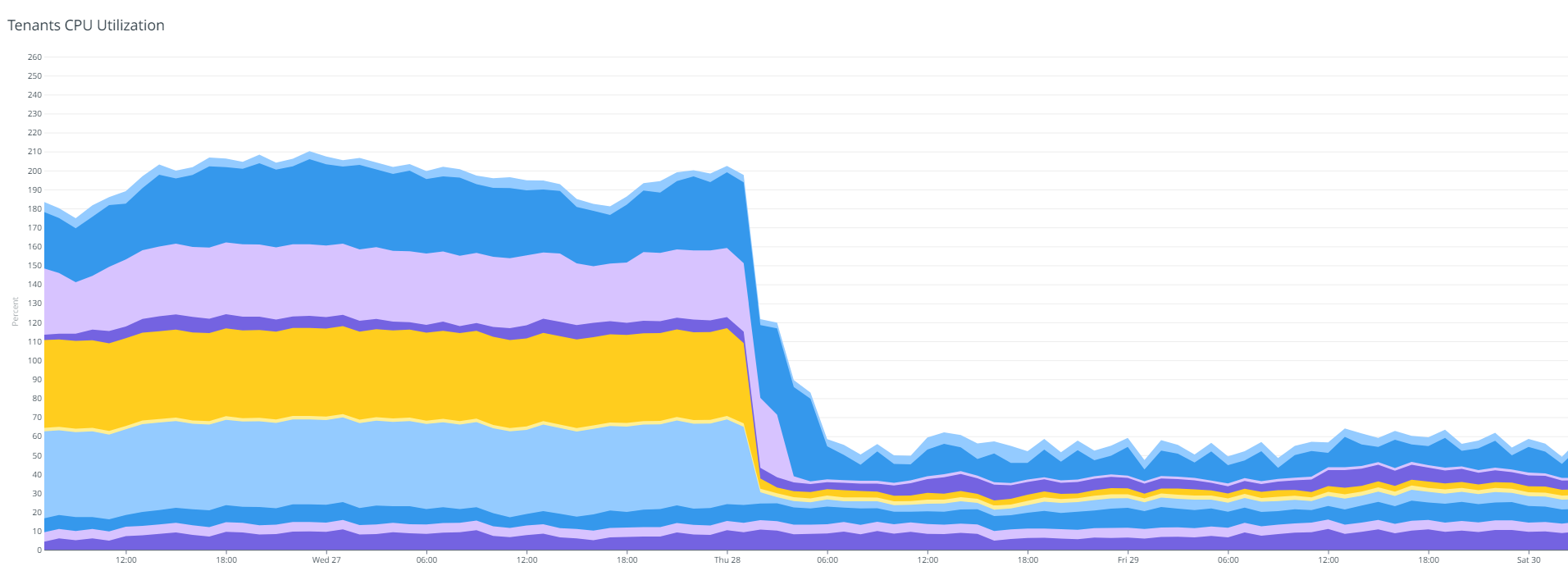

With bundle consolidation, OCES launched Policy Publication v3. This release not only resolved the bundle activation latency issue, but also reduced the CPU and memory utilization of the OPA tenants, paving the way to reduce operational costs.

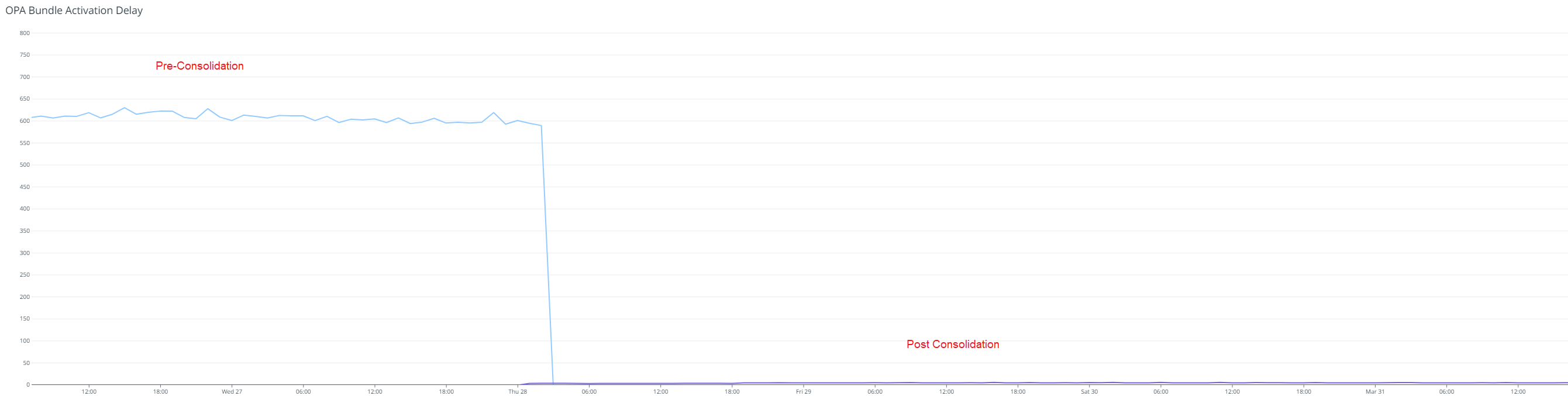

Figure 8: With bundle consolidation, the bundle activation lag reduced from ~10 minutes to near-zero. This means that the bundles are activated instantly upon download.

Figure 9: Bundle consolidation reduced the CPU utilization of OCES OPA tenants

Other Enhancements:

- The OCES bundle generation service was optimized to generate new reference data bundles only if the reference data was modified.

- The OCES Rego pipeline extensively supports unit testing of the policies including test coverage gates, test coverage reports and Git submodules integration to include dependencies e.g. common Rego libraries.

Notable Trade-offs

Decision latency vs Memory utilization: To minimize the authorization decision latency, we load the bundles in OPA memory. This decision favors low latency over infrastructure costs.

Data freshness vs Resource consumption: OPA polls S3 every minute to check for fresh bundles. This frequency results in high CPU and network usage, an increased bundle download and activation overhead; however it reduces the staleness of Rego policies and reference data. This decision favors data freshness over resource consumption costs.

Outcome

The iterative optimizations in OCES, particularly the introduction of bundle discovery, bundle signing and bundle consolidation, have significantly enhanced the efficiency, security, and performance of the OPA policy bundle delivery process. It demonstrates the effectiveness of the strategies implemented to overcome the initial challenges.

See https://www.gs.com/disclaimer/global_email for important risk disclosures, conflicts of interest, and other terms and conditions relating to this blog and your reliance on information contained in it.

Solutions

Curated Data Security MasterData AnalyticsPlotTool ProPortfolio AnalyticsGS QuantTransaction BankingGS DAP®Liquidity Investing¹ Real-time data can be impacted by planned system maintenance, connectivity or availability issues stemming from related third-party service providers, or other intermittent or unplanned technology issues.

Transaction Banking services are offered by Goldman Sachs Bank USA ("GS Bank") and its affiliates. GS Bank is a New York State chartered bank, a member of the Federal Reserve System and a Member FDIC. For additional information, please see Bank Regulatory Information.

² Source: Goldman Sachs Asset Management, as of March 31, 2025.

Mosaic is a service mark of Goldman Sachs & Co. LLC. This service is made available in the United States by Goldman Sachs & Co. LLC and outside of the United States by Goldman Sachs International, or its local affiliates in accordance with applicable law and regulations. Goldman Sachs International and Goldman Sachs & Co. LLC are the distributors of the Goldman Sachs Funds. Depending upon the jurisdiction in which you are located, transactions in non-Goldman Sachs money market funds are affected by either Goldman Sachs & Co. LLC, a member of FINRA, SIPC and NYSE, or Goldman Sachs International. For additional information contact your Goldman Sachs representative. Goldman Sachs & Co. LLC, Goldman Sachs International, Goldman Sachs Liquidity Solutions, Goldman Sachs Asset Management, L.P., and the Goldman Sachs funds available through Goldman Sachs Liquidity Solutions and other affiliated entities, are under the common control of the Goldman Sachs Group, Inc.

Goldman Sachs & Co. LLC is a registered U.S. broker-dealer and futures commission merchant, and is subject to regulatory capital requirements including those imposed by the SEC, the U.S. Commodity Futures Trading Commission (CFTC), the Chicago Mercantile Exchange, the Financial Industry Regulatory Authority, Inc. and the National Futures Association.

FOR INSTITUTIONAL USE ONLY - NOT FOR USE AND/OR DISTRIBUTION TO RETAIL AND THE GENERAL PUBLIC.

This material is for informational purposes only. It is not an offer or solicitation to buy or sell any securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO. Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant. This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client's account should or would be handled, as appropriate investment strategies depend upon the client's investment objectives.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA): This marketing communication is disseminated by Goldman Sachs Asset Management B.V., including through its branches ("GSAM BV"). GSAM BV is authorised and regulated by the Dutch Authority for the Financial Markets (Autoriteit Financiële Markten, Vijzelgracht 50, 1017 HS Amsterdam, The Netherlands) as an alternative investment fund manager ("AIFM") as well as a manager of undertakings for collective investment in transferable securities ("UCITS"). Under its licence as an AIFM, the Manager is authorized to provide the investment services of (i) reception and transmission of orders in financial instruments; (ii) portfolio management; and (iii) investment advice. Under its licence as a manager of UCITS, the Manager is authorized to provide the investment services of (i) portfolio management; and (ii) investment advice.

Information about investor rights and collective redress mechanisms are available on www.gsam.com/responsible-investing (section Policies & Governance). Capital is at risk. Any claims arising out of or in connection with the terms and conditions of this disclaimer are governed by Dutch law.

To the extent it relates to custody activities, this financial promotion is disseminated by Goldman Sachs Bank Europe SE ("GSBE"), including through its authorised branches. GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank (Sonnemannstrasse 20, 60314 Frankfurt am Main, Germany) and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht, BaFin) (Graurheindorfer Straße 108, 53117 Bonn, Germany; website: www.bafin.de) and Deutsche Bundesbank (Hauptverwaltung Frankfurt, Taunusanlage 5, 60329 Frankfurt am Main, Germany).

Switzerland: For Qualified Investor use only - Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited ("GSAMHK") or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) ("GSAMS") nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited and in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

- Goldman Sachs Asset Management, LP (GSAMLP), Goldman Sachs & Co. LLC (GSCo), pursuant ASIC Class Order 03/1100; regulated by the US Securities and Exchange Commission under US laws.

- Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), pursuant to ASIC Class Order 03/1099; regulated by the Financial Conduct Authority; GSI is also authorized by the Prudential Regulation Authority, and both entities are under UK laws.

- Goldman Sachs Asset Management (Singapore) Pte. Ltd. (GSAMS), pursuant to ASIC Class Order 03/1102; regulated by the Monetary Authority of Singapore under Singaporean laws

- Goldman Sachs Asset Management (Hong Kong) Limited (GSAMHK), pursuant to ASIC Class Order 03/1103 and Goldman Sachs (Asia) LLC (GSALLC), pursuant to ASIC Instrument 04/0250; regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

FOR DISTRIBUTION ONLY TO FINANCIAL INSTITUTIONS, FINANCIAL SERVICES LICENSEES AND THEIR ADVISERS. NOT FOR VIEWING BY RETAIL CLIENTS OR MEMBERS OF THE GENERAL PUBLIC

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law ("FIEL"). Also, any description regarding investment strategies on or funds as collective investment scheme under Article 2 paragraph (2) item 5 or item 6 of FIEL has been approved only for Qualified Institutional Investors defined in Article 10 of Cabinet Office Ordinance of Definitions under Article 2 of FIEL.

Interest Rate Benchmark Transition Risks: This transaction may require payments or calculations to be made by reference to a benchmark rate ("Benchmark"), which will likely soon stop being published and be replaced by an alternative rate, or will be subject to substantial reform. These changes could have unpredictable and material consequences to the value, price, cost and/or performance of this transaction in the future and create material economic mismatches if you are using this transaction for hedging or similar purposes. Goldman Sachs may also have rights to exercise discretion to determine a replacement rate for the Benchmark for this transaction, including any price or other adjustments to account for differences between the replacement rate and the Benchmark, and the replacement rate and any adjustments we select may be inconsistent with, or contrary to, your interests or positions. Other material risks related to Benchmark reform can be found at https://www.gs.com/interest-rate-benchmark-transition-notice. Goldman Sachs cannot provide any assurances as to the materialization, consequences, or likely costs or expenses associated with any of the changes or risks arising from Benchmark reform, though they may be material. You are encouraged to seek independent legal, financial, tax, accounting, regulatory, or other appropriate advice on how changes to the Benchmark could impact this transaction.

Confidentiality: No part of this material may, without GSAM's prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

GSAM Services Private Limited (formerly Goldman Sachs Asset Management (India) Private Limited) acts as the Investment Advisor, providing non-binding non-discretionary investment advice to dedicated offshore mandates, involving Indian and overseas securities, managed by GSAM entities based outside India. Members of the India team do not participate in the investment decision making process.